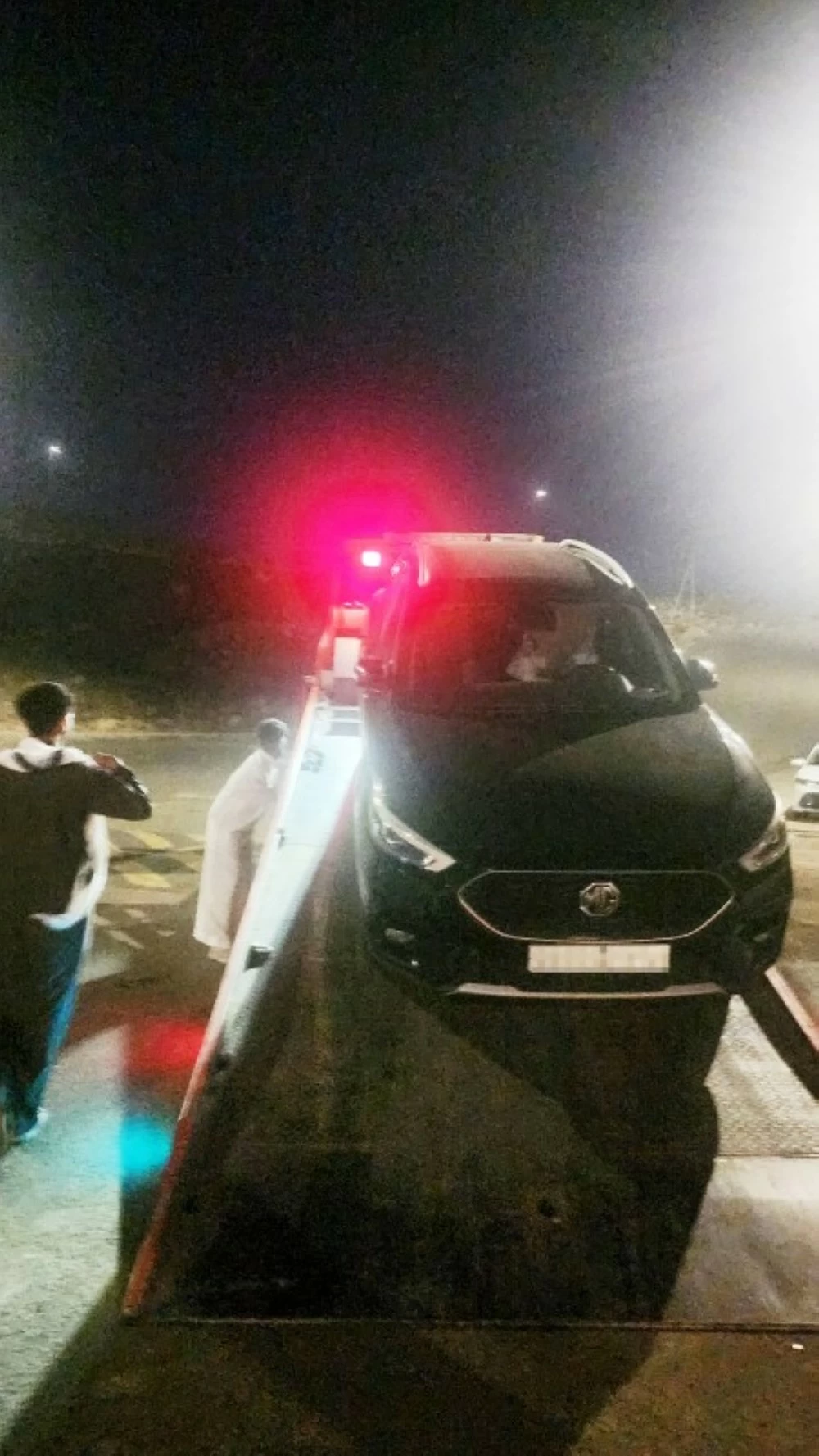

عاد «أبو راكان» من المسجد الحرام بعد أداء العمرة للراحة في أحد الفنادق بحي العزيزية تاركاً متعلقاته الخاصة من «الإثباتات» والنقود في سيارته الخاصة، على أمل أن يغادر مكة بعد صلاة العصر، وحين حمل حقائبه تأهباً للسفر فوجئ بعدم وجود سيارته في موقعها! فبدأ رحلة البحث عنها في الشوارع، وبعد عناء طويل استقر به الحال في الدخول إلى أحد المحلات التجارية المزودة بكاميرات المراقبة ليكتشف حضور أشخاص بسيارة نقل (سطحة) حملت سيارته إلى جهة غير معلومة!

صادف ذلك يوم إجازة (جمعة) وكان عليه الانتظار ليقطع مسافة من مكة المكرمة إلى حجز السيارات في الجموم على طريق جدة بحثاً عن سيارته المفقودة.

معاناة «أبو راكان» يتعرض لها مئات العديد من مستخدمي نظام الإيجار المنتهي بالتمليك، فحجة البنوك في تبرير سلوكها أن المستفيد وقع على هذه الإجراءات عند الشراء.

جعلوني «مسلوب الهوية»!

عبدالرحمن الغامدي يستغرب الطريقة التي يتم من خلالها سحب السيارات في حال تعثّر السداد، ويصفها بأنها أشبه بطريقة «الأفلام».. أحدهم يراقب الموقع ومنزل صاحب السيارة لحين وصول سيارة (السطحة) ثم تحميلها والهرب من الموقع

ويتساءل: طالما إجراءات السحب سليمة لماذا كل هذه الطرق الملتوية.. لماذا لا يتم التواصل مع صاحب السيارة حتى يأخذ متعلقاته من سيارته بدلاً من تركه «مسلوب الهوية»

في المقابل، يرى مصدر في أحد البنوك وشركات التقسيط، أنهم يعتمدون على سند تنفيذ يوقع عند الشراء ويطبق على الجميع في حالة تأخير السداد.

ضوابط «المركزي» في «السحب»

المحامي والمستشار القانوني مشاري عبدالرحمن الثبيتي قال لـ«عكاظ»: إنه حرصاً على ديمومة العلاقة التمويلية بين من المؤجر والمستأجر، شرعت الجهة المعنية المتمثلة في «البنك المركزي السعودي» ضوابط وأحكاماً بهدف وضع العلاقة التعاقدية التمويلية ضمن إطار تنظيمي محدد بما يكفل التزام كل من الأفراد والمؤسسات بالمعايير والإجراءات اللازمة إلى جانب تعزيز الاستقرار المالي والأداء وتحقيق أعلى مستويات التنظيم لضمان استمرارية الخدمات المطلوبة ولذلك أصدر البنك المركزي تعميماً في 1442/06/12هـ يُعنى بضوابط وإجراءات طلب وإصدار مستخرجات السند التنفيذي لعقد الإيجار التمويلي المسجل، الذي نظّم فيه إجراءات طلب وإصدار مستخرج شهادة سحب الأصل المؤجر (المركبة)، ونظمت المادة السادسة منه حالات إصدار مستخرج شهادة سحب الأصل المؤجر، وذلك في حال تخلف المستأجر عن سداد الدفعات الشهرية لمدة ثلاثة أشهر متتالية أو خمسة أشهر متفرقة على أن يؤخذ في عين الاعتبار؛ كون تلك الضوابط قيدت المؤجر باتخاذ خطوات مسبقة لا يجوز للمؤجر تجاوزها أو انتهاكها، تتمثل في إشعار المستأجر من خلال اجراء اتصال موثق بحسب الهاتف أو البريد الإلكتروني المنصوص عليه في العقد بوجوب سداد الدفعات المتأخرة، على أن يتم فيه بيان كل من (اسم المؤجر والجهة المعنية بتحصيل المتأخرات وأن يكون تقديم الطلب لإصدار شهادة سحب الأصل المؤجر بعد 15 يوماً من إشعار المستأجر بوجوب سداد تلك الدفعات المتعثرة، وفي حالة انتهاء عقد الإيجار التمويلي وعدم امتلاك المستأجر للأصل المؤجر أو إعادته للمؤجر وذلك بشرط التحقق من انتهاء مدة العقد، إضافة إلى تعذّر نقل ملكية المركبة للمستأجر على ضوء ما تقدم يقع على عاتق المؤجر تزويد المستأجر بنموذج معتمد لمحضر جرد المركبة، وذلك من خلال الاتصال الموثق بعقد الإيجار التمويلي بتمكين المستأجر من استلام الموجودات والممتلكات العائدة له كافة مع إعداد بيان يثبت فيه استلام المستأجر لها.

متى يتم الإتلاف؟

المحامي الثبيتي يضيف: أنه حال كانت للمتعلقات قيمة مادية فيتم التصرف بها بحسب الأحوال إذا كانت ممّا لا يخشى عليه التلف، فتحفظ مدة 30 يوماً وبعد ذلك يتم تقييمها من مقيم معتمد ويتم بيعها وإيداع قيمتها لدى الجهة المختصة، وأما إذا كانت الموجودات ما يخشى عليه التلف فيتم تقييمها مباشرة ويتم بيعها، وعلى خلاف ما سبق إذا كانت تلك الموجودات ممّا ليس لها قيمة مادية فيتم حفظها مدة 30 يوماً ومن ذلك يتم إتلافها بموجب محضر، كما جرى التنويه بعدم جواز المؤجر التصرف في الأصل المؤجر، ومن ذلك على سبيل المثال لا الحصر: (بيع المركبة أو إقفال العقد) وذلك قبل انقضاء 15 يوماً من تاريخ استرداد المركبة، على أن يتم إشعار المستأجر بالمبالغ المشغولة في ذمته وكافة المستندات اللازمة لتسليمه الأصل المؤجر، وخلاصة ما سبق أن الضوابط شرعت لحماية المتعاملين فيه خصوصاً (المستأجر)؛ كونه الطرف الأضعف في العلاقة التمويلية وفي المقابل تفرض عقود الإيجار التمويلية التزامات على (المؤجر) يهدف منها الحفاظ على حقوق المستأجر

كم هي قيمة السيارة؟

الاقتصادي عمر العمران وخلال حديثه لـ«عكاظ» قال: إن الإيجار المنتهي بالتمليك من أحد أركانه لا بد أن تكون السيارة مؤمناً عليها تأميناً شاملاً خلال سريان العقد، فالسيارة خلال العقد تكون مرهونة للبنك؛ لذلك عندما يحصل شخص على سيارة من البنك المنتهي تكون هناك قيمة تقديرية لكل سنة بمعنى أن العقد الممتد لخمس سنوات يكون السعر للعام الأول أعلى من السنة التي تليها ثم التي تليها فالأرقام يضعها البنك لا القيمة السوقية فقد تكون السيارة جيدة وسعرها يتم تخفيضه لأقل من قيمتها السوقية والمشكلة من الأساس أن البنك وضع قيمة منخفضة بغرض تقليل قيمة التأمين الشامل!

“Abu Rakan” returned from the Grand Mosque after performing Umrah to rest in one of the hotels in the Al-Aziziyah neighborhood, leaving his personal belongings, including “identifications” and money, in his private car, hoping to leave Mecca after the Asr prayer. When he picked up his bags in preparation for travel, he was shocked to find that his car was no longer in its spot! He began a search for it in the streets, and after a long struggle, he ended up entering one of the shops equipped with surveillance cameras to discover that individuals had arrived in a tow truck and taken his car to an unknown location!

This incident occurred on a holiday (Friday), and he had to wait to cover the distance from Mecca to the car impound lot in Al-Jamoom in search of his lost car.

Abu Rakan's ordeal is faced by hundreds of users of the lease-to-own system, as banks justify their actions by claiming that the beneficiary signed these procedures at the time of purchase.

They made me “devoid of identity”!

Abdulrahman Al-Ghamdi is astonished by the method used to repossess cars in case of payment default, describing it as akin to a “movie” scenario... someone monitors the location and the owner's house until the tow truck arrives, then loads the car and flees the scene.

He wonders: As long as the repossession procedures are legitimate, why all these convoluted methods... why not communicate with the car owner so they can retrieve their belongings from the car instead of leaving them “devoid of identity”?

On the other hand, a source from one of the banks and installment companies stated that they rely on an execution bond signed at the time of purchase, which applies to everyone in case of payment delays.

Central Bank Regulations on “Repossession”

Lawyer and legal advisor Mishari Abdulrahman Al-Thubaiti told “Okaz”: In order to maintain the financing relationship between the lessor and the lessee, the concerned authority represented by the “Saudi Central Bank” has established regulations and provisions aimed at placing the financing contractual relationship within a specific regulatory framework that ensures compliance by both individuals and institutions with the necessary standards and procedures, in addition to enhancing financial stability and performance and achieving the highest levels of organization to ensure the continuity of the required services. Therefore, the Central Bank issued a circular on 12/06/1442 AH concerning the regulations and procedures for requesting and issuing extracts of the execution bond for the registered lease contract, which organized the procedures for requesting and issuing an extract of the certificate for repossession of the leased asset (the vehicle). Article six of it organized the cases for issuing an extract of the certificate for repossession of the leased asset, in the event that the lessee fails to pay the monthly installments for three consecutive months or five sporadic months, taking into consideration that these regulations require the lessor to take prior steps that the lessor cannot bypass or violate, which include notifying the lessee through a documented phone call or email specified in the contract regarding the necessity of paying the overdue installments, stating both (the name of the lessor and the entity responsible for collecting the arrears), and that the request for issuing the certificate for repossession of the leased asset should be submitted after 15 days from notifying the lessee of the necessity of paying those overdue installments. In the event of the expiration of the lease contract and the lessee not owning the leased asset or returning it to the lessor, provided that it is verified that the contract period has ended, in addition to the impossibility of transferring ownership of the vehicle to the lessee, the lessor is obliged to provide the lessee with an approved form for the vehicle inventory report, through the documented contact of the lease contract, enabling the lessee to receive all assets and properties belonging to them, along with preparing a statement confirming the lessee's receipt of them.

When is destruction permitted?

Lawyer Al-Thubaiti adds: If the belongings have material value, they are to be handled according to the circumstances; if they are not at risk of damage, they are to be kept for 30 days, after which they are evaluated by an accredited appraiser and sold, with the proceeds deposited with the relevant authority. If the assets are at risk of damage, they are to be evaluated immediately and sold. Conversely, if those assets have no material value, they are to be kept for 30 days and then destroyed according to a report. It has also been noted that the lessor is not permitted to dispose of the leased asset, including but not limited to: (selling the vehicle or closing the contract) before the expiration of 15 days from the date of repossessing the vehicle, and the lessee must be notified of the amounts owed to them and all necessary documents to hand over the leased asset. In summary, the regulations were established to protect the parties involved, especially the (lessee), as they are the weaker party in the financing relationship, while financing lease contracts impose obligations on the (lessor) aimed at preserving the rights of the lessee.

What is the value of the car?

Economist Omar Al-Omaran, during his conversation with “Okaz,” stated that one of the pillars of the lease-to-own system is that the car must be comprehensively insured during the contract period. The car is mortgaged to the bank during the contract; therefore, when a person obtains a car from the bank, there is an estimated value for each year. This means that a contract extending for five years will have a higher price for the first year than the following year, and so on. The figures are set by the bank, not the market value. The car may be in good condition, but its price is reduced to below its market value, and the problem fundamentally lies in the bank setting a low value to reduce the comprehensive insurance cost!